Markets

What to know:

- Amplification, which sounds rather like a jazz band warming up, is defined as debt plus preferred equity divided by bitcoin reserves, and it has recently risen to a dizzying 33%, creating a veritable mountain of senior claims poised to pounce on the equity below. One could say MSTR holders might need to invest in helmets.

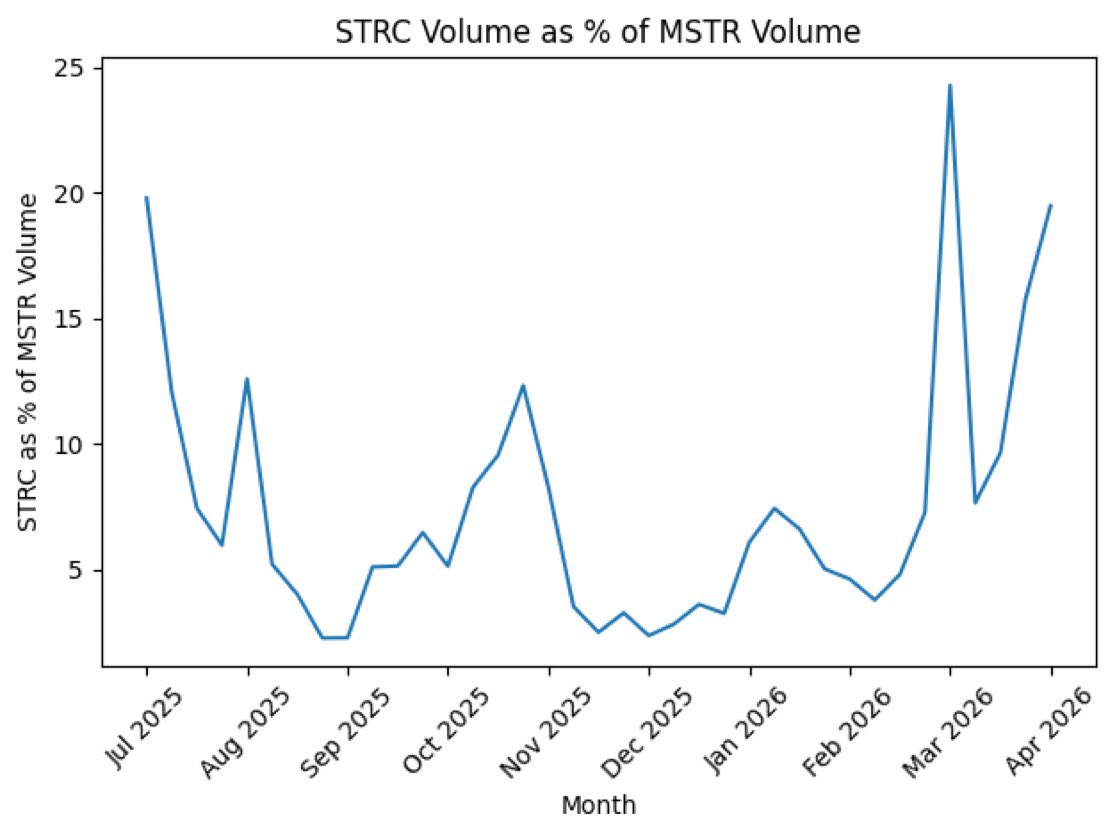

- The trading of STRC preferred stock has surged from a shy wallflower in the single digits to a boisterous 20% of MSTR volume. It appears we have quite the party crasher on our hands!

- With higher amplification and the increasingly cheeky STRC activity, managing this structural concoction has become akin to herding cats, enhancing downside sensitivity and reliance on equity issuance that can weigh heavily on performance relative to bitcoin. Talk about a balancing act!

Stock market investors, bless their hearts, may be blissfully overlooking one rather intriguing metric nestled comfortably within the Strategy (MSTR), the grandest publicly traded holder of bitcoin: the capital market measure known as amplification. A delightful mouthful, isn’t it?

This amplification, dear reader, compares the size of the Michael Saylor-led company’s total debt and its collection of debt-like trinkets, such as preferred stock, to its rather impressive stash of 766,970 BTC. As amplification rises-much like the tension at a poorly planned dinner party-it adds more risk to the company, making the common stock as jittery as a cat at a dog show when bitcoin price movements occur.

Investors have been rather engrossed with the price of bitcoin and the multiple to net asset value (mNAV) premium when sizing up the company. But should amplification, currently flirting with the 33% mark, continue to escalate, it might very well become the top dog in the risk department.

At the apex of Strategy’s capital structure sits convertible debt, roughly $8.25 billion worth of the most senior claim, like a prim and proper butler overseeing the household. Below that, a motley crew of preferred stocks-STRC, STRK, STRD, and STRF-holds court with approximately $10.3 billion in notional value, according to the ever-reliable MSTR dashboard. At the bottom of this raucous pile dwells common equity, MSTR, which must absorb all the residual upside and downside like a seasoned amateur at a buffet.

Now, STRC has been crafted with great care to serve as the primary vehicle for bitcoin accumulation for the company, sitting rather comfortably senior to equity and junior to debt. It graciously offers an 11.5% annual dividend, dispersed monthly in cash, because who doesn’t love a little monthly surprise in the post?

Once a lonely whisper in the low single digits relative to MSTR, STRC has gallantly surged to around 20% on a weekly basis, occasionally spiking above 25%. According to the MSTR dashboard, last Friday saw MSTR trade $1.7 billion-well below its $2.5 billion 30-day average-while STRC strutted its stuff with $526 million, nearly double its $259 million average, accounting for almost 50% of MSTR’s volume in a single day. Bravo!

The heightened STRC activity makes it increasingly challenging to manage amplification without resorting to the common stock equity issuance, which can weigh down performance compared to bitcoin. Over the past 30 days, while the bitcoin price has remained fairly stable, MSTR has taken a tumble, falling 11%. Quite the dramatic performance, wouldn’t you agree?

At lower amplification, MSTR behaves somewhat like leveraged BTC, but at these higher levels, it becomes a veritable circus to manage, especially with about $1.12 billion in annual obligations looming like an unexpected guest at a dinner party.

Read More

- Gold Rate Forecast

- Brent Oil Forecast

- Silver Rate Forecast

- USD BRL PREDICTION

- NEAR PREDICTION. NEAR cryptocurrency

- USD CNY PREDICTION

- Hong Kong Delays First Stablecoin Licenses as HKMA Tightens Compliance Rules

- Is Bitcoin About To Throw A September Tantrum Before The Q4 Party? 🎢💸

- Is Trust Wallet’s Tokenized RWA Feature the Future of Finance or Just Hype?

- Hanke’s Hilarious Takedown: US Economy in the Dumps, Iran Calling the Shots!

2026-04-13 13:26