on-chain value received by centralized services, retail-sized on-chain value received by centralized services, on-chain value received by DeFi protocols, and institutional-sized on-chain value received by centralized services. Chainalysis, with their customary diligence, ranks each country across these pillars, weighs the results by such considerations as population and purchasing power, and then takes a geometric mean to produce a normalized 0-1 score. They assure us that their inputs encompass “hundreds of millions of cryptocurrency transactions and more than 13 billion web visits,” though they modestly acknowledge the limitations of web-traffic-based geolocation. 📊✨

Methodologically, 2025 marks a notable pivot. Chainalysis, in a fit of prudence, “removed the retail decentralized finance (DeFi) sub-index” after concluding it over-weighted a “relatively niche behavior,” and added a new institutional activity lens capturing transfers over $1 million, reflecting the post-ETF surge in professional participation. The aim, they write, is a “fuller view of global crypto engagement, capturing both bottom-up (retail) and top-down (institutional) activity.” One cannot help but admire their ambition, though one wonders if they might not be biting off more than they can chew. 🧐📈

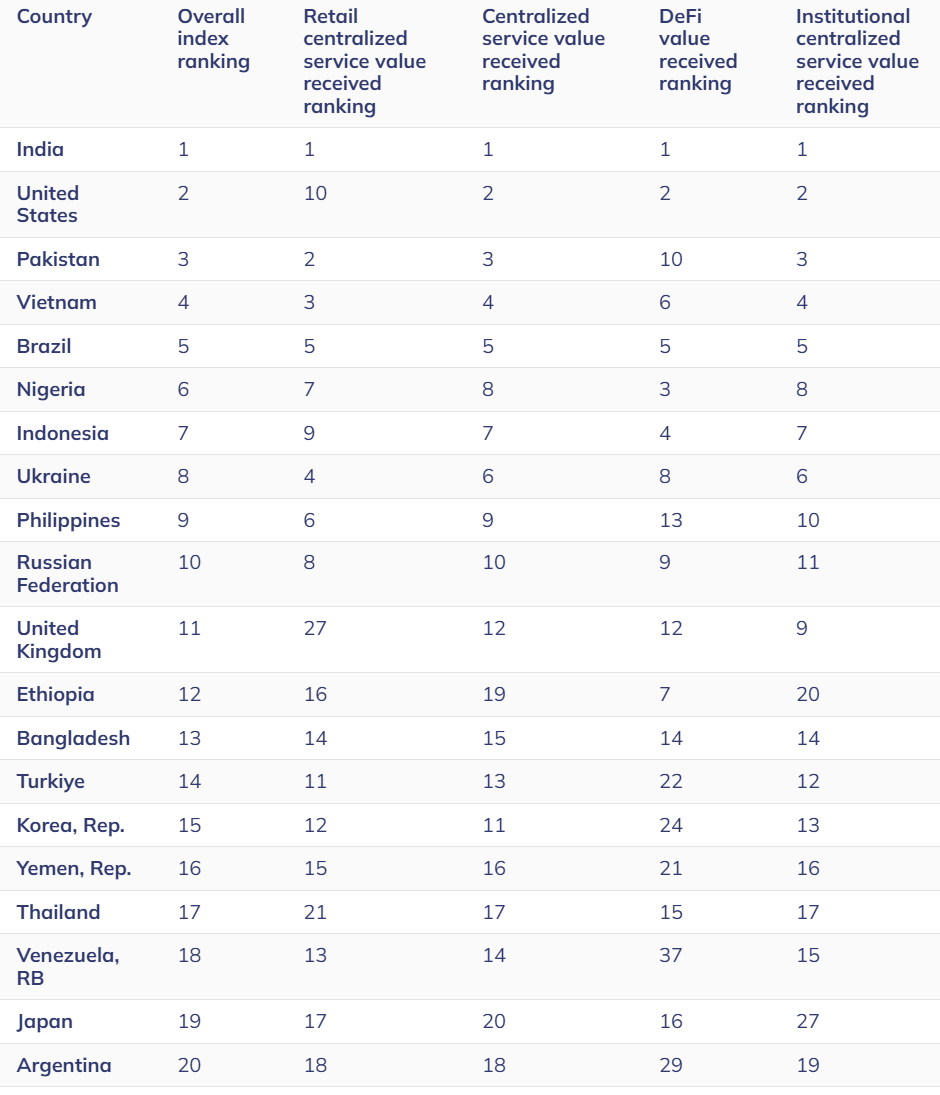

The headline table underscores Asia’s weight. India sits first overall and first across all four underlying categories; Pakistan and Vietnam join it in the global top four, while Brazil rounds out the top five. Nigeria, Indonesia, Ukraine, and the Philippines rank sixth through ninth, with the Russian Federation at ten and the United Kingdom at eleven. Notably, Ethiopia and Yemen enter the top twenty at twelfth and sixteenth, respectively, while Japan ranks nineteenth and Argentina twentieth. Chainalysis attributes the regional momentum to a surge in both centralized and decentralized usage across major APAC markets. One can only imagine the bustle and clamor in those quarters! 🌏🚀

Regional flow data deepen that picture. Over the twelve months to June 2025, APAC’s on-chain value received jumped 69% year over year-from roughly $1.4 trillion to $2.36 trillion-making it the fastest-growing region. Latin America followed at 63% growth and Sub-Saharan Africa at 52%. In absolute terms, Europe and North America still dominate, receiving about $2.6 trillion and $2.2 trillion respectively over the period; North America’s activity grew 49% amid renewed institutional participation, while Europe rose 42%. MENA expanded by 33%. One is tempted to ask if Europe and North America are merely resting on their laurels, but perhaps it is unkind to suggest as much. 🌍📉

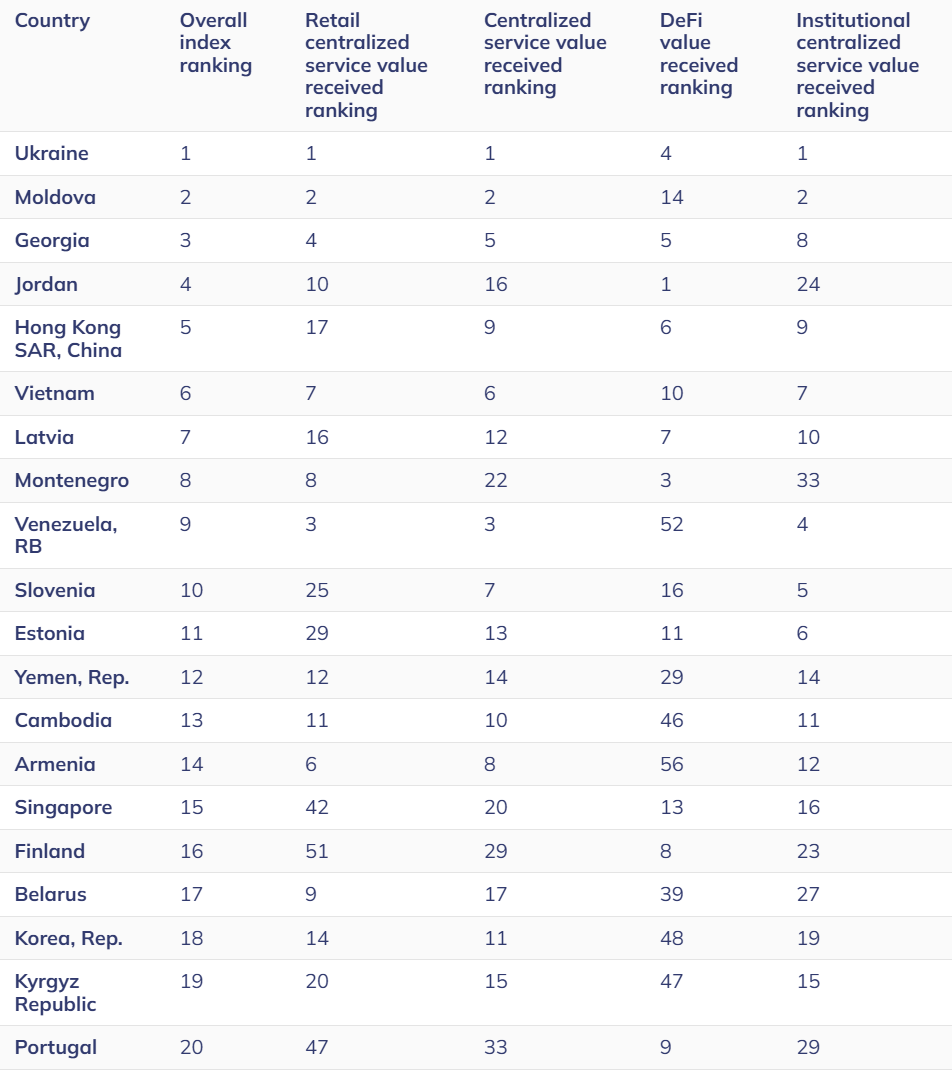

A population-adjusted cut of the index tells a different story, highlighting where crypto has penetrated most deeply relative to country size. On that basis, Eastern Europe is ascendant: Ukraine ranks first, Moldova second, and Georgia third, ahead of Jordan and Hong Kong SAR. Chainalysis links the region’s leadership to economic uncertainty, distrust in banks, and high technical literacy that make crypto attractive for wealth preservation and cross-border transfers. Vietnam again appears near the top in this view, underscoring its broad-based retail engagement. One cannot help but marvel at the resourcefulness of these nations in the face of adversity. 🌍💪

Stablecoins remain the connective tissue of global crypto commerce. Chainalysis finds that USDT and USDC continue to dwarf peers in transaction volume, with USDT processing over $1 trillion per month between June 2024 and June 2025 and USDC ranging roughly from $1.24 trillion to $3.29 trillion monthly, even as newer, more regulated or regionally tailored tokens accelerate. EURC’s monthly volume, for example, rose from about $47 million to more than $7.5 billion over the period, while PYUSD climbed from roughly $783 million to $3.95 billion. One is left to wonder if these stablecoins are the new gold standard, or merely a passing fancy. 💸🔗

The firm situates these flows within shifting rulesets-MiCA’s stablecoin regime in the EU and US legislative momentum exemplified by the GENIUS Act-alongside expanding merchant rails from payments giants and card-linked integrations by major crypto platforms. It is a complex web indeed, and one can only hope that it does not become hopelessly entangled. 🕸️⚖️

Crucially, the report analyzes the fiat “on-ramp” into crypto across centralized exchanges. “Bitcoin leads by a wide margin,” Chainalysis writes, accounting for over $4.6 trillion in fiat purchase volume from July 2024 to June 2025-more than double Layer-1 tokens ex-BTC and ETH (about $3.8 trillion), with stablecoins at $1.3 trillion and altcoins around $540 billion. The United States is the largest national on-ramp at more than $4.2 trillion, followed by South Korea above $1 trillion and the European Union just under $500 billion; Bitcoin’s share of fiat inflow is especially pronounced in the UK and EU at roughly 47% and 45%. One cannot help but feel a twinge of envy at such prodigious sums. 💰🚀

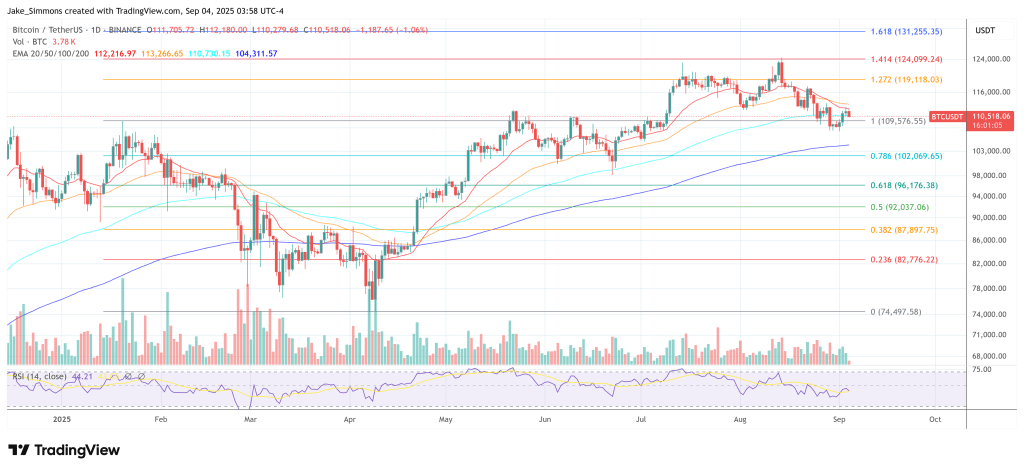

At press time, Bitcoin traded at $110,518. Whether this is a cause for celebration or consternation, I leave to the reader’s discretion. 📈💹

Read More

- TRUMP PREDICTION. TRUMP cryptocurrency

- Gold Rate Forecast

- USD CNY PREDICTION

- Brent Oil Forecast

- Bitcoin’s Dramatic Fall Puts Strategy’s Holdings in Crisis Mode! What Happens Next?

- Larry David on Pakistan & Kyrgyzstan’s Crypto Love Affair 🤦♂️

- Ant Group’s “ANTCOIN”: Will It Conquer Crypto? Find Out What’s Next!

- Bitcoin Signals Recession…” but then contrast with the data. Also, mention the potential upside. Let me check character count. “Bitcoin Signals Recession, But Data Says Otherwise – Bullish Opportunity Ahead?” That’s 78 characters. Maybe shorten “Bullish

- Kraken & Deutsche Börse: A Match Made in Financial Limbo! 🦑💼

- Is Dogwifhat’s $1.15 Dream Still Alive? 🐶💰

2025-09-04 14:30