What to know:

Stay informed about the world of cryptocurrency with Crypto Long & Short, our weekly newsletter designed for serious investors. Subscribe here to receive it directly in your inbox every Wednesday.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Alec Beckman on why BTC-backed lending is not a crypto story, but a capital efficiency story.

- Serena Sebastiani on how stablecoins aren’t a crypto product; they’re becoming the settlement infrastructure global finance forgot.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- “Ethena’s Solana lending markets cross $1B in 4 days” in Chart of the Week.

Thanks for joining us!

-Alexandra Levis

Expert Insights

Bitcoin-backed loans belong in the cost-of-capital conversation

By Alec Beckman, VP of the Americas, Psalion

As a researcher in this space, I’m not focused on *if* people should buy Bitcoin, but rather on how those who already own it – or advise clients who do – can use it more effectively. Specifically, I keep wondering: if a client has significant debt, why aren’t we considering Bitcoin-backed loans as a financing option? Professionals dealing with debt routinely compare things like collateral, interest rates, fees, and loan terms. Bitcoin-backed loans deserve the same careful evaluation – it’s just another form of collateral to consider.

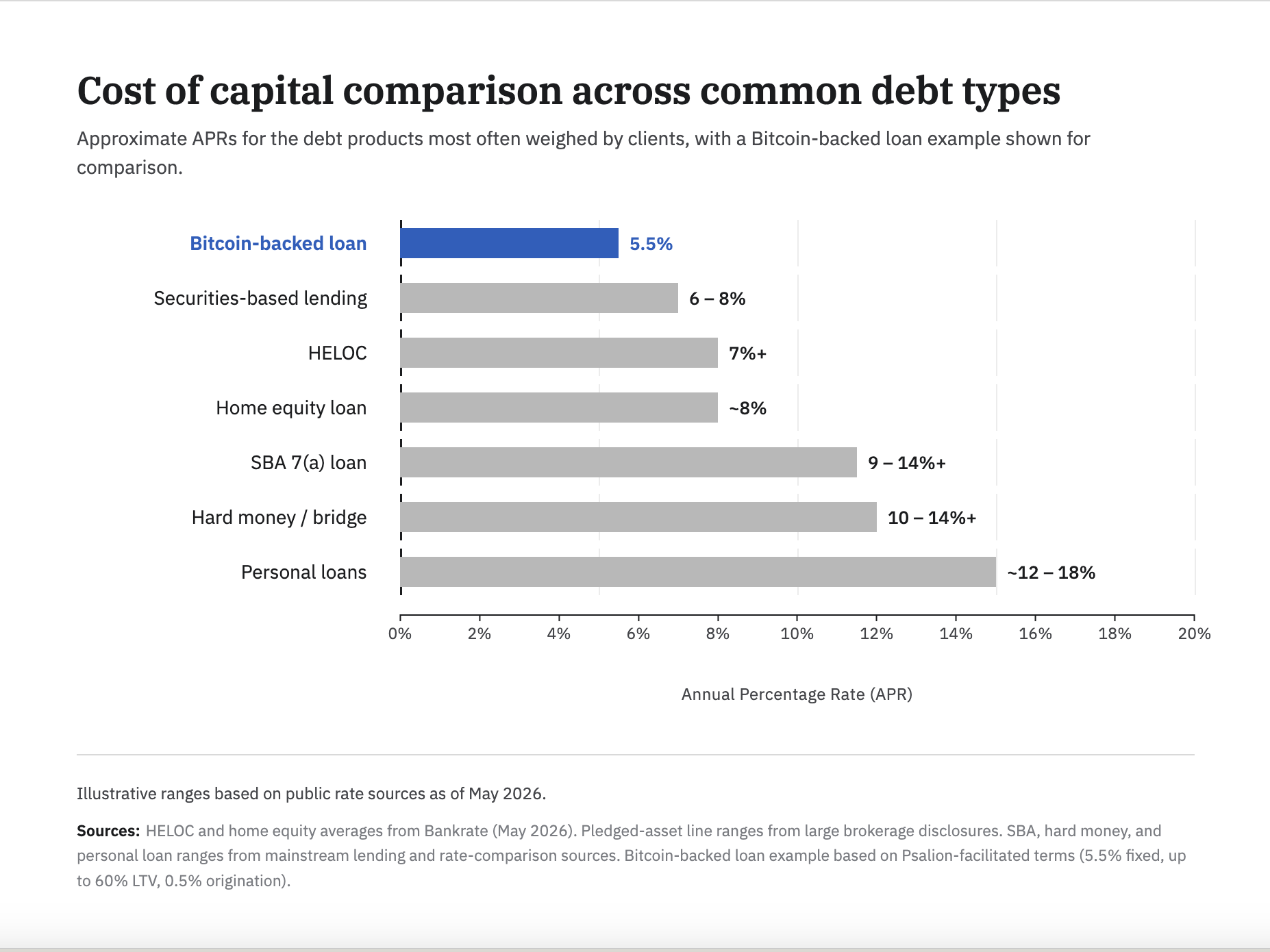

Borrowers have several debt options, each with its own drawbacks. Home equity lines of credit (HELOCs) are linked to your home’s value and usually have variable interest rates, currently exceeding 7% for many. Short-term loans like hard money and bridge loans offer speed but are expensive, typically ranging from 10% to 14% plus additional fees. Securities-based lending is relatively efficient but requires significant investment assets and usually starts around 6% to 8% interest. Personal loans generally fall between 13% and 15%. While SBA loans can be helpful, they involve considerable paperwork, time, and overall costs.

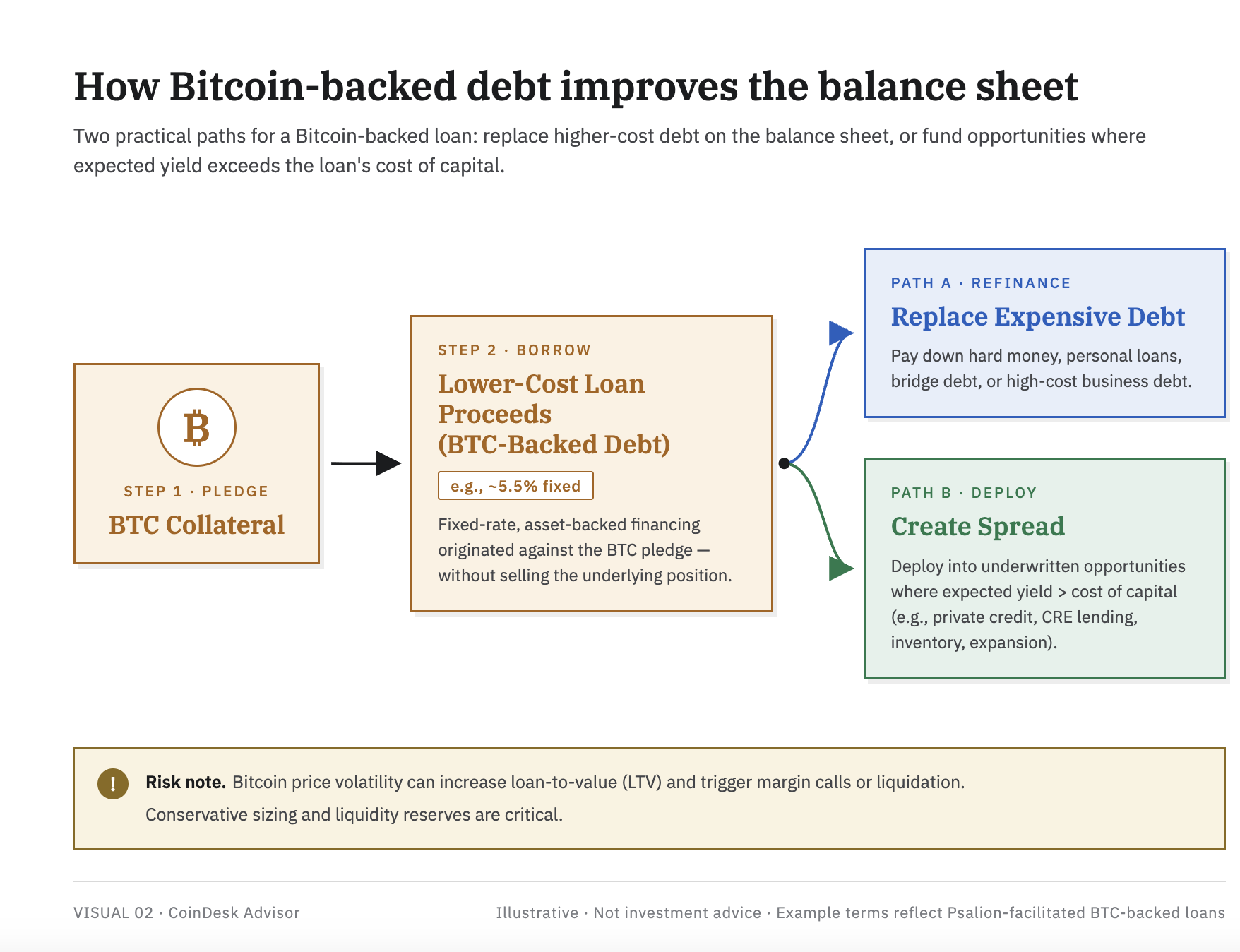

Bitcoin-backed loans simply use Bitcoin as collateral instead of traditional assets. Borrowers put up Bitcoin, receive funds in dollars or stablecoins, and repay the loan according to the agreed terms. Because Bitcoin is easily bought, sold, and tracked, these loans are quite transparent. While interest rates still differ across lenders, we’re starting to see more competitive options. For instance, at Psalion, we offer fixed-rate Bitcoin-backed loans at 5.5% APR, up to 60% loan-to-value, with a one-time 0.5% origination fee. This demonstrates that Bitcoin-backed lending deserves consideration alongside other types of debt.

The interest rate is the most important factor. For Bitcoin owners, the question isn’t *if* they should borrow, but *where* to borrow from. They could borrow against assets like a house, business, or investments, or even use their Bitcoin as collateral. If borrowing against Bitcoin results in a lower overall interest rate compared to their current debts, it can lower their total borrowing costs.

Let’s talk about fees. Loans from private investors often come with extra upfront costs. SBA loans can have guarantee fees, closing costs, and advisor fees. Personal loans might have higher interest rates built in. Bitcoin-backed loans with lower fees can significantly improve the overall cost.

Traditional loans can be slow and complicated, requiring lots of paperwork like proof of income and property appraisals. Bitcoin-backed loans are different – they focus first on the value of the Bitcoin used as collateral, which can be verified and tracked quickly. This faster access to funds isn’t just more convenient; it can make a real difference when you need to refinance, buy something, pay taxes, or cover a short-term financial gap, potentially improving the financial outcome.

Financial advisors need to pay attention to Bitcoin because more of their clients are now holding it as an asset. Often, this Bitcoin just sits unused while the client continues to pay high interest rates on other debts. If advisors can help clients borrow against their Bitcoin to pay off those more expensive debts, they can strengthen the client’s overall financial position without requiring a sale – and potentially avoiding capital gains taxes.

Another common strategy is ‘yield on spread,’ where investors, entrepreneurs, and business owners seek opportunities to earn more from their investments than it costs them to fund those investments. This often involves areas like private loans, commercial property lending, company inventory, or growing their business operations.

Taking out a loan using Bitcoin as collateral can be a good strategy if you understand both the potential profits and the risks involved with the Bitcoin itself.

This risk is genuine. Bitcoin’s price can change quickly and significantly. If the price drops enough, it could force borrowers to add more collateral or even sell their Bitcoin to cover the loan. This sale could result in a taxable event. This type of loan isn’t suitable for everyone; it’s best for borrowers who understand Bitcoin’s price swings, have enough readily available funds, and borrow cautiously, keeping the loan amount well below the maximum allowed.

If you already have bitcoin and outstanding debts, using it as collateral for a loan isn’t about crypto—it’s about getting more value from what you already own. Overlooking this option could mean missing out on lower borrowing costs or a profitable financial opportunity.

Principled Perspectives

Stablecoins are now infrastructures

By Serena Sebastiani, chief strategy officer and head of government and regulatory affairs, Fuze

There’s a kind of financial friction that becomes invisible when you live inside it long enough.

From New York or London, cross-border payments work. From Nairobi, Jakarta or Almaty, they don’t.

A small business in Nairobi sends a payment to a supplier in Karachi. The transfer takes three business days to complete. During this process, the money goes through two intermediary banks, incurs various fees, and is subject to currency exchange costs and security checks. Both the buyer and supplier factor these extra costs into the price of the goods and adjust payment terms to compensate.

Here’s how money moves along some of the world’s busiest trade routes: between the Gulf and South Asia, within Africa, from the CIS to the Middle East and North Africa (MENA), and for remittances in Southeast Asia.

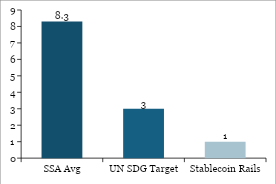

Consider the $136 billion shortfall in trade finance for small and medium-sized businesses in Africa, plus the $100 billion sent home by people working abroad each year. Now expand that to other key trade routes like the Gulf to South Asia, countries of the former Soviet Union to the Middle East and North Africa, and within Southeast Asia. Also, remember that sending money to Sub-Saharan Africa is still very expensive – averaging 8.3% per transaction, nearly three times the recommended global target of 3%. Currently, some modern payment systems are already operating at costs below 1%. This isn’t just about making small improvements; it’s a fundamental problem in some of the world’s fastest-growing economies.

SWIFT was originally created for big banks and large international transactions. It still works well for those purposes. However, smaller payments – like those made to suppliers in Nairobi, money sent from Riyadh to Manila, or trades between cities like Almaty and Istanbul – have been relying on a system designed for a different, larger-scale economic world.

That’s the gap stablecoins are moving into, and they’re not a product but real plumbing.

Chart 1: The Remittance Cost Gap

Sources: World Bank (Q1 2025); UN SDG 10.c; Transak / Operational corridor data

What we observe from the ground

I’ve been talking with regulators and those who run the financial markets in rapidly growing areas, and a clear trend has emerged: the people dealing with the practical challenges are the most open-minded when it comes to solutions. They’re the ones actively working to incorporate stablecoins into how the current financial system works.

In Kigali, Rwanda, the focus isn’t simply on getting people to use cryptocurrency. Instead, the country’s central bank began testing a digital currency (CBDC) in February, prioritizing its ability to work with other countries’ systems. A new proposed law divides virtual assets into two categories: payment-focused stablecoins, overseen by the central bank, and investment assets, regulated by the Capital Markets Authority. Furthermore, a recent agreement with Kenya to streamline fintech licensing is being used as a model for the wider East African Community. This demonstrates a deliberate and well-planned regulatory framework being built to address specific needs and understanding of the local market.

This isn’t just about Rwanda; across Africa, mobile money is now the primary way people manage their finances. With over a billion accounts and nearly everyone included in the financial system in places like Rwanda, this system has taken years to develop. However, mobile money struggles with transactions across borders. Stablecoins can easily fill this need, not by replacing traditional currencies, but by providing a faster and more efficient way to settle payments.

The same logic, four corridors

Middle East

The UAE Central Bank’s new rules for payment tokens, like stablecoins, view them as essential parts of the payment system, not just risky investments. This approach lets banks issue stablecoins in UAE Dirham (AED) that people can use to pay for things directly. It also allows banks and fintech companies to build services using stablecoins without having to worry about every transaction as a potential debt. This means stablecoin payments in the Gulf region are happening within a secure, regulated environment.

CIS markets

In countries like Kazakhstan, Uzbekistan, and Georgia, people often turn to U.S. dollars because their local currencies can be unstable and traditional banks don’t always offer reliable access to foreign currency. Stablecoins are essentially a new way for people in these countries to use dollars. This creates an opportunity for businesses to provide secure and compliant access to these digital dollars, with robust custody and reserve standards to ensure long-term stability.

Southeast Asia

In Southeast Asia, people prioritize low costs and fast transactions. For sending money between countries like the Gulf region, Indonesia, or the Philippines, using stablecoins removes the need to have funds ready in advance and dramatically speeds up the process – from taking days to just minutes, often less than 20, and available 24/7. Businesses are already seeing operational cost savings of 40% to 80%.

I spoke with regulators, banks, and fintech companies in these markets. The key question we’re trying to answer is: how can we increase the use of stablecoins and benefit everyday families?

Africa

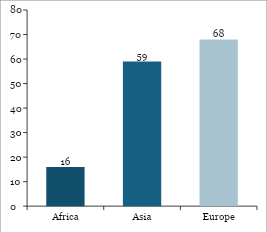

Sending money across borders is costly, but it’s also crucial to improve trade *within* Africa. Currently, only 16% of Africa’s trade happens between African countries, compared to 68% in Europe and 59% in Asia. The African Continental Free Trade Area (AfCFTA) has created the legal framework for a $3.4 trillion market, but the systems for actually making payments haven’t developed quickly enough. Chinese businesses buying goods from Africa are already using USDT for transactions because it’s better suited to their needs. To expand this successfully and ensure it’s widely used, it’s essential to make sure all transactions are done legally and through secure, reliable systems.

Chart 2: Intra-Regional Trade Share — Africa vs Peers

Sources: UNCTAD / AfDB / WTO; World Bank / African Union (AfCFTA projection)

Stablecoins are infrastructure

Banks and financial technology companies currently see stablecoins mostly as products for customers. However, the real potential lies in using them as a foundational infrastructure, especially for sending money internationally (remittances) and for business payments. This includes areas like managing company funds, paying suppliers, and settling foreign exchange transactions. Stablecoins can significantly speed up these processes and lower costs – reducing times from days to minutes and fees from significant amounts to fractions of a percent. Importantly, well-designed stablecoin systems offer clear and traceable compliance records through on-chain monitoring, wallet identification, and automated reporting – something traditional money transfer methods can’t provide. The data generated by these systems can also help rebuild banking relationships in markets where financial institutions have reduced their services due to risk concerns.

Solving the friction

To make the infrastructure work reliably as it grows, we still need to address a few key things: clear rules for maintaining reserves and allowing withdrawals, better cooperation between countries overseeing the system, and ways to ensure anti-money laundering and counter-terrorism financing laws work together across borders.

We’re actively addressing these issues, with a greater focus on rapidly growing markets rather than already-developed ones.

Through working with regulators, I’ve found a successful approach involves three key elements: first, a licensing system that allows regulators to learn as the market develops; second, rules that are tailored to the size and risk level of each institution; and third, agreements between countries that allow companies to easily meet compliance requirements across borders.

From where I’m sitting, the regions that would benefit most from this infrastructure aren’t passively waiting for international guidelines – they’re already actively developing their own solutions. The key question for global organizations is whether they’ll help shape this emerging landscape, or simply try to catch up to what’s already being built.

Headlines of the Week

Francisco Rodrigues

This week saw significant steps forward for bringing traditional finance onto the blockchain. A key bill aiming to modernize market structures passed a major vote, JPMorgan expanded its capabilities for tokenizing assets, and investment firms are working on ways to speed up the process of handling investor withdrawals. Meanwhile, Solana has been steadily improving its technology to attract larger, institutional investors.

- Clarity Act clears U.S. Senate committee, on its way to a final test in Congress: Chairman Tim Scott secured a 15-9 bipartisan vote with Democrats Gallego and Alsobrooks crossing over, though unresolved law enforcement and government-ethics provisions still stand between the bill and a floor vote before the summer recess.

- JPMorgan files to launch new tokenized fund as Wall Street tokenization race heats up: The Ethereum-based JLTXX fund, run through JPMorgan’s Kinexys blockchain unit, is structured to satisfy GENIUS Act stablecoin reserve requirements — landing days after BlackRock filed for its own tokenized Treasury vehicle.

- BlackRock, Janus Henderson tokenized funds get instant redemptions with new $1 billion facility: Grove’s Basin facility advances stablecoin liquidity against approved redemptions from BlackRock’s $2.2 billion BUIDL and Janus Henderson’s $1.1 billion JTRSY, targeting the multi-day settlement gap that has held back the $15 billion tokenized Treasury market.

- Mike Novogratz’s Galaxy receives New York BitLicense for institutional crypto push: NYDFS cleared GalaxyOne Prime NY to serve hedge funds, RIAs and family offices on a $9 billion platform, making Galaxy only the second firm to win a BitLicense in 2026 after Strike.

- Solana is shedding its memecoin reputation as big banks move billions into its ecosystem: A Messari report shows Solana’s tokenized RWA market cap jumped 43% QoQ to $2.01 billion, with BlackRock’s BUIDL, Ondo, Franklin Templeton and a Citigroup-PwC trade finance PoC live on the network, alongside payments integrations from Visa, Stripe, PayPal and Western Union.

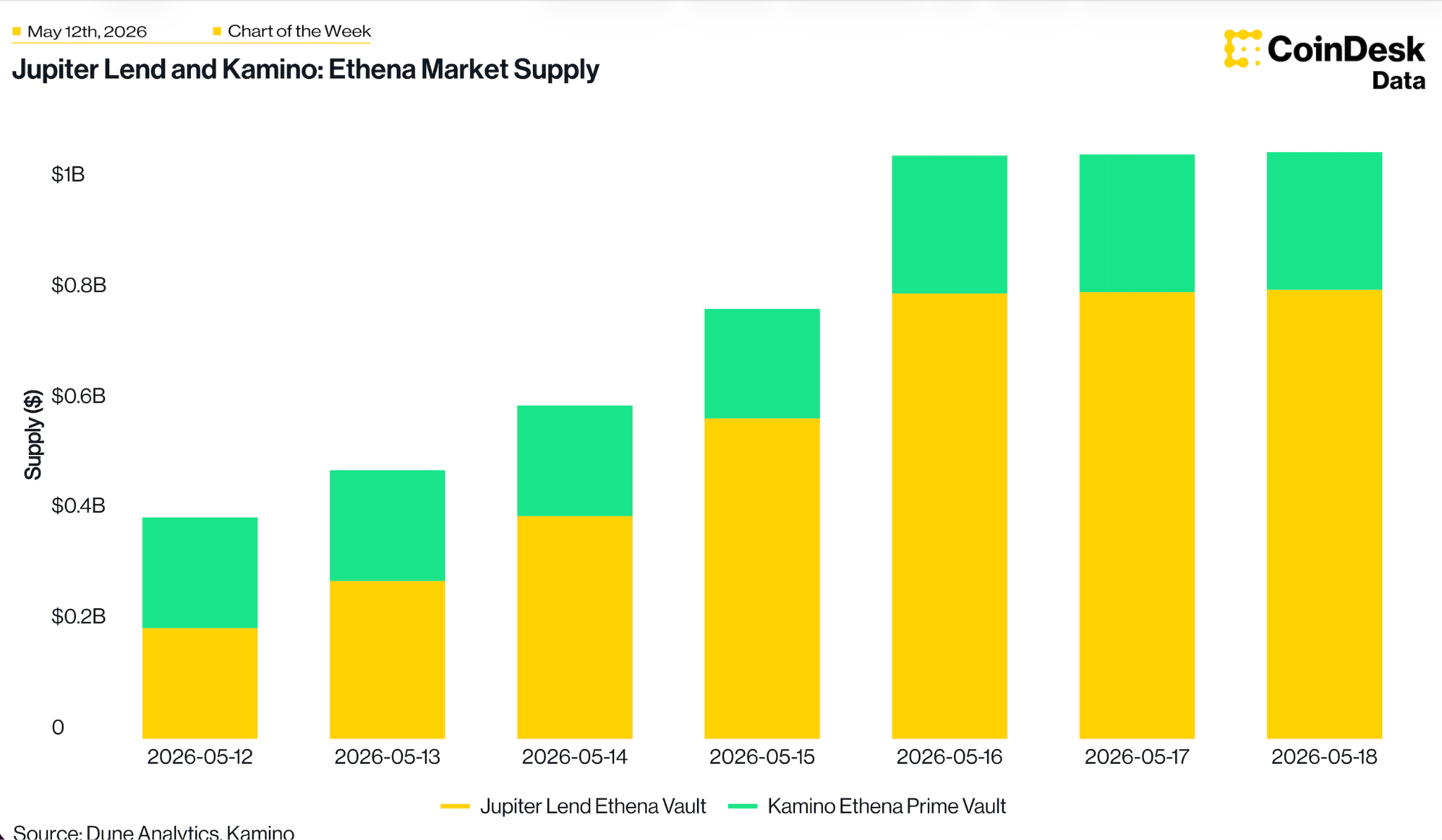

Chart of the Week

Ethena’s Solana lending markets cross $1B in 4 days

The total amount of USDe and USDG supplied through Bitwise-managed markets on Jupiter Lend and Kamino Ethena grew significantly, from $401 million on May 12th to $1.06 billion by May 16th. This increase was primarily due to activity on Jupiter Lend, where supply jumped from $201 million to $812 million. Meanwhile, the amount held in Kamino’s Ethena Prime vault remained relatively stable at around $250 million.

Listen. Read. Watch. Engage.

- Listen: Did you hear? CoinDesk’s May 2026 Exchange Benchmark report from CoinDesk Research was released last week. The standards have been raised and our research team breaks down the ratings.

- Watch: Videos are live from Consensus 2026 by CoinDesk. Rewatch a favorite global thought leader onstage or watch for the first time!

- Engage: CoinDesk will be at the Women in Digital Assets Forum (WIDAF) in NYC on June 3. Let’s connect onsite!

Want to stay informed? Get the newest cryptocurrency news and market insights from CoinDesk at coindesk.com and coindesk.com/institutions.

Read More

- CNY JPY PREDICTION

- GBP USD PREDICTION

- USD TRY PREDICTION

- SUI PREDICTION. SUI cryptocurrency

- USD JPY PREDICTION

- USD HKD PREDICTION

- M PREDICTION. M cryptocurrency

- USD BRL PREDICTION

- Gold Rate Forecast

- USD RUB PREDICTION

2026-05-20 19:49