a sharp 11% drop has thrown a staggering $8.6 billion of BTC options into the realm of the out‑of‑the‑money, destined to expire like a stale pastry.

That figure is roughly 80 percent of the $10.6 billion of contracts slated to expire on June 26, per Deribit’s own ledger. These dollars are not cash, but the notional open interest – the estimated value of contracts that traders have stitched together at this very moment.

Options are contraptions where a cynical trader bets the price will swing one way or the other by a certain date. One call is a hopeful “the price will rise!” while a put is a more pragmatic “the price will fall!”.

Being “in‑the‑money” means the option is already a winner if exercised now; “out‑of‑the‑money” means it’s prolifically losing and will vanish when the clock strikes expiry, just like a winter morning after a punchline.

Quarterly expiries, such as June 26, are the Russian doll’s hinge: when the lid opens, a furious reshuffling by traders and makers swirls into heightened volatility. The effect is magnified when the market’s posture is as lopsided as a sardonic chandelier that has been propped against a cracked wall.

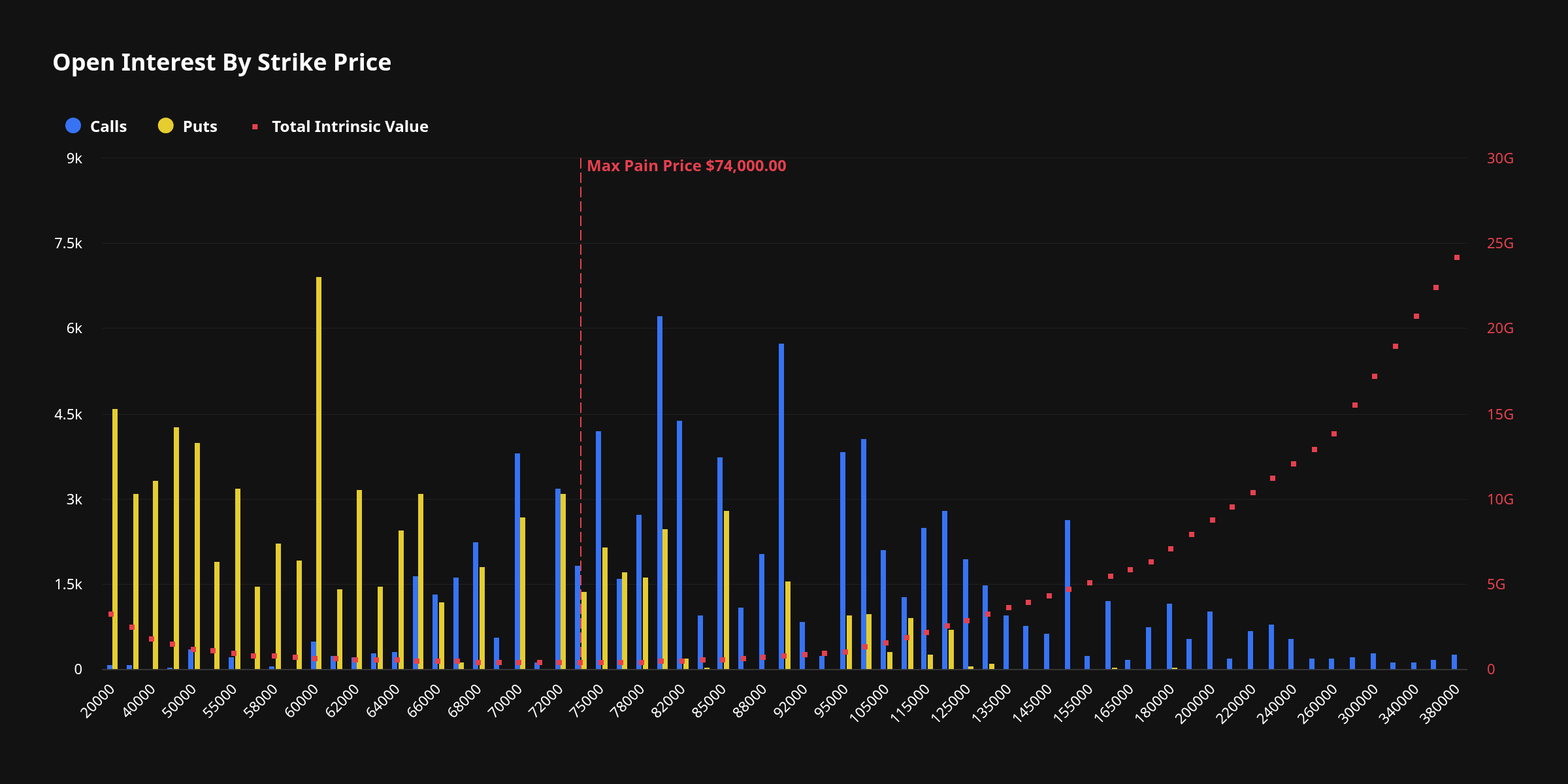

With merely about 20 percent of the $10.6 billion in open interest securely in‑the‑money, and a staggering 80 percent languishing out‑of‑the‑money, the marketplace teeters on a sharp, pivoting edge that could tumble into a churning whirl as players scramble to re‑balance their positions.

And the tale does not end there.

Max Pain and the Put‑Call Ratio – a Sadistic Dance

The tale whispers that the “max pain” for June 26 hovers at $74,000 – a 14 percent jump over Bitcoin’s scalp‑tingling current spot near $65,000.

Max pain is the price point where the largest congregation of contracts would simply expire into oblivion. The theory, inherited from old Wall Street lullabies, suggests that as expiry draws close, the underlying will “murmur” at that price, as makers correct their missteps like a scribe correcting ink drift.

While the “max pain” specter is revered in traditional markets, its dominion over crypto is a subject of vigorous debate. Still, if the whisper holds true, Bitcoin may be nudged back up to $74,000 in the days ahead – a celestial bounce or simply a prank played by unnamed pranksters.

Meanwhile, the put‑to‑call ratio sits at a modest 0.87 – 87,156 call contracts challenge 76,241 put contracts across a notional interest exceeding $10.6 billion. The slight supremacy of calls hints at a mad dancer’s curiosity, while the narrow balance underscores how unsettled traders truly are.

Open interest concentrates on two pivotal strikes. The $60,000 put harbors about $450 million of exposure, acting as a tender support all week. The $80,000 call, carrying roughly $406 million, stands as an intimidating sky‑high hurdle, like an overripe apple on a tree that Admittation loves to pick.

All told, these expiry mechanics might carve a meaningful path into Bitcoin’s forthcoming price future, and like a Chekhovian theatre, we’ll be waiting for the final act to see if the audience applauds or sighs.

Read More

- Crypto Exchange Bullish Shares Make a Splash: $102 Debut Beats IPO Price by a Mile!

- Bitcoin Spectacle: Strive buys 2,500 BTC as markets sigh

- Why Two Chinas Are Playing Games With Crypto Like It’s Monopoly 😱

- Crypto Drama: EDGE Token Plummets, ZachXBT Calls BS on Insider Shenanigans

- Bitcoin’s Gonna Crash? Maybe. Who Cares? Buy the Dip, You Coward!

- CNY JPY PREDICTION

- USD CNY PREDICTION

- USD RUB PREDICTION

- USD BRL PREDICTION

- EUR PHP PREDICTION

2026-06-17 14:56