Ah, the grand theater of institutional finance! For decades, it danced to the slow, ponderous rhythm of correspondent banking-a waltz of one to three days, weekends off, and the occasional curtsy to inefficiency. But lo, the stage has changed, and the players now wear the masks of stablecoins.

In the year 2025, stablecoins pirouetted to the tune of $33 trillion, a sum that would make even Visa blush. JP Morgan, ever the aristocrat, settled debts in USDC on Solana, while Visa, not to be outdone, shuffled $3.5 billion in USDC through the halls of American banks. PayPal, the nouveau riche, launched its own stablecoin across 70 markets, declaring, “We too shall have our moment in the sun!”

And so, the settlement layer, once a staid affair, has been transformed into a carnival of digital tokens. This tale, dear reader, is not merely of numbers and networks but of the souls who built the rails upon which institutional finance now gallops-rails that, like the threads of a great tapestry, are woven with both ingenuity and hubris.

Ten Trillion in a Month: The Institutions Take the Reins

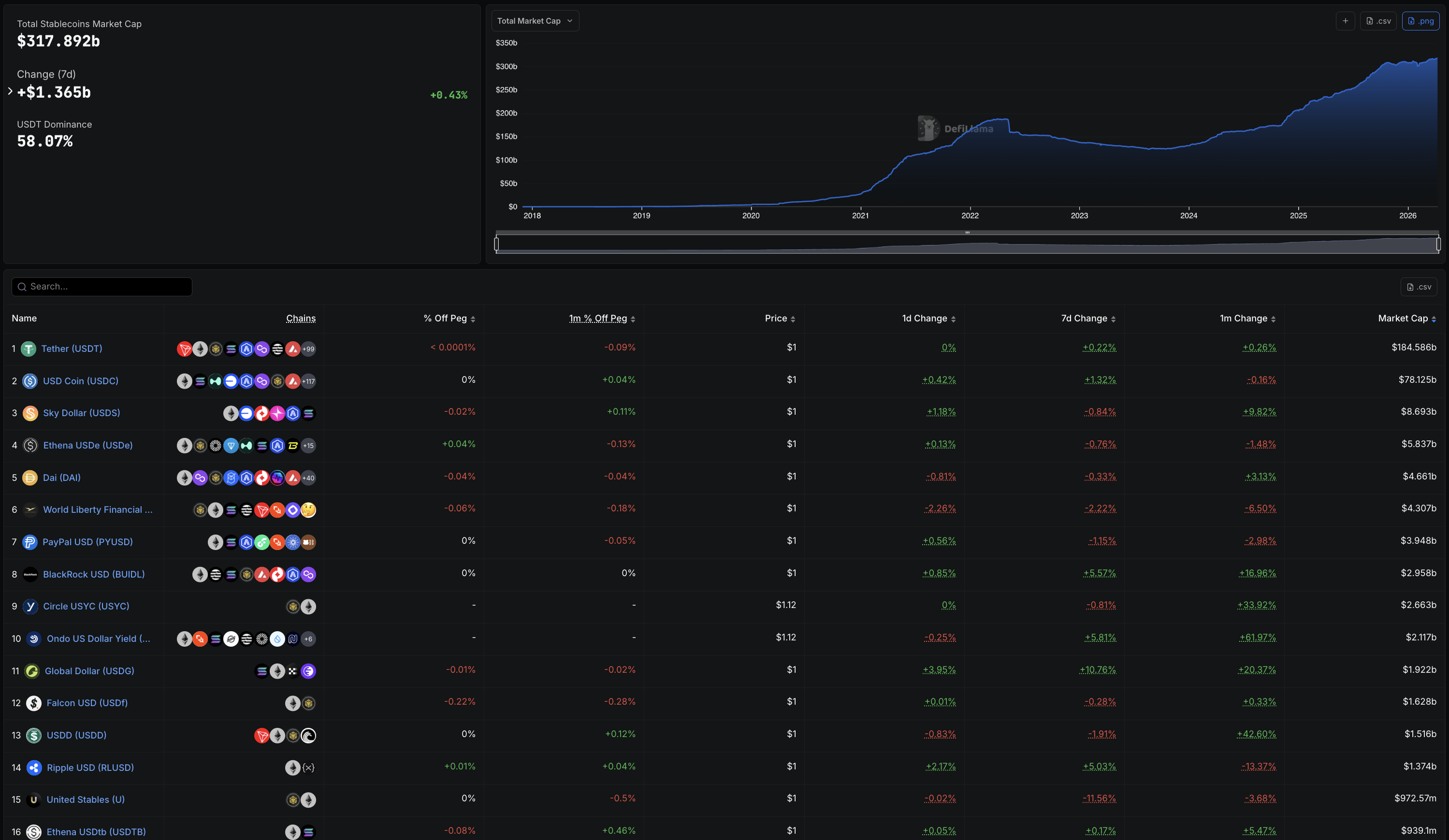

Behold, the stablecoin market cap swelled to $317.89 billion by April 2026, a far cry from its modest $125 billion in early 2024. The GENIUS Act, signed with great fanfare in mid-2025, bestowed upon stablecoins a federal framework, and the institutions, ever pragmatic, embraced it with open arms. The growth since? Vertical, like a rocket launched by a madman with a penchant for disruption.

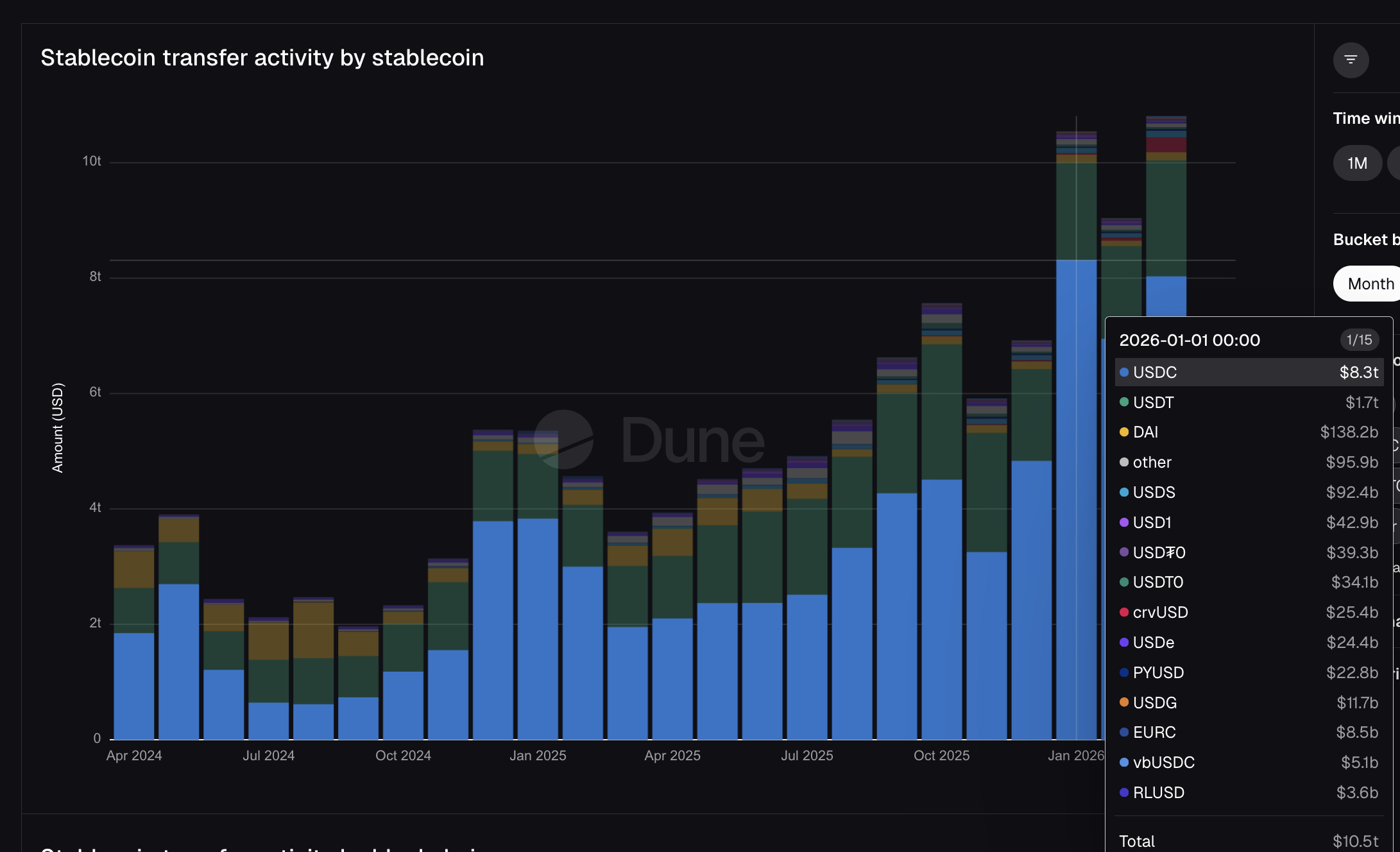

Dune Analytics, that tireless chronicler of digital deeds, reveals that stablecoins transferred $10.5 trillion in January 2026 alone. To put this in perspective, Visa, the old guard, processed $16.7 trillion in fiat payments across its entire fiscal year of 2025. Mastercard, not to be outshone, managed $10.6 trillion in the same period. Yet, in a single month, stablecoins on public blockchains approached what Mastercard’s fiat network toiled to achieve in a year. Ah, the irony of progress!

The DefiLlama leaderboard, that great ledger of digital wealth, tells a tale of institutional conquest. PayPal’s PYUSD sits at #7, with a supply of $3.95 billion. BlackRock’s BUIDL, ever the titan, holds #8 at $2.96 billion. And Mastercard’s USDG, the fruit of its partnership with the Global Dollar Network, rests at #11 with $1.92 billion. These are not the tokens of crypto natives, no. These are the stablecoins of the old world, now dancing alongside USDT and USDC, like aristocrats at a plebeian ball.

USDC, that stalwart of stability, moved $8.3 trillion in January, nearly five times USDT’s $1.7 trillion, despite being but a fraction of its size in supply. USDT dominates holdings, but USDC dominates movement. And why? Because USDC is the chosen one-the stablecoin of Visa’s settlement, JP Morgan’s debt deals, and Stripe’s infrastructure. The institutional settlement layer, it seems, runs on a single token, minted by Circle. A monopoly, you say? Nay, merely the natural order of things in this brave new world.

Meanwhile, PayPal’s PYUSD moved $22.8 billion, and Mastercard’s USDG shuffled $11.7 billion. The TradFi stablecoins are now visible on the volume charts, and every one of them traces back to just two minters. Circle and Paxos, the modern-day alchemists, turning fiat into digital gold.

Proof of Talk is joining us as co-host of the Institutional 100 Awards.

The most respected Awards.

At a spectacular venue!📍Louvre Palace, Paris

🗓️ 2-3 June, 2026The BeInCrypto x @proofoftalk Institutional 100 Awards ceremony will recognize the top institutions building the…

– BeInCrypto (@beincrypto) April 9, 2026

Two Minters, One Rail, and the Banks Are Left in the Dust

Circle and Paxos, the twin pillars of this new order, mint the tokens that move trillions. Circle, with its USDC, moved $8.3 trillion in January. Paxos, ever versatile, mints PYUSD for PayPal and USDG for the Global Dollar Network, anchored by Mastercard, Robinhood, Kraken, and DBS Bank. Between them, every major TradFi stablecoin integration traces back to one of these two entities. A duopoly, you say? Nay, merely efficiency in action.

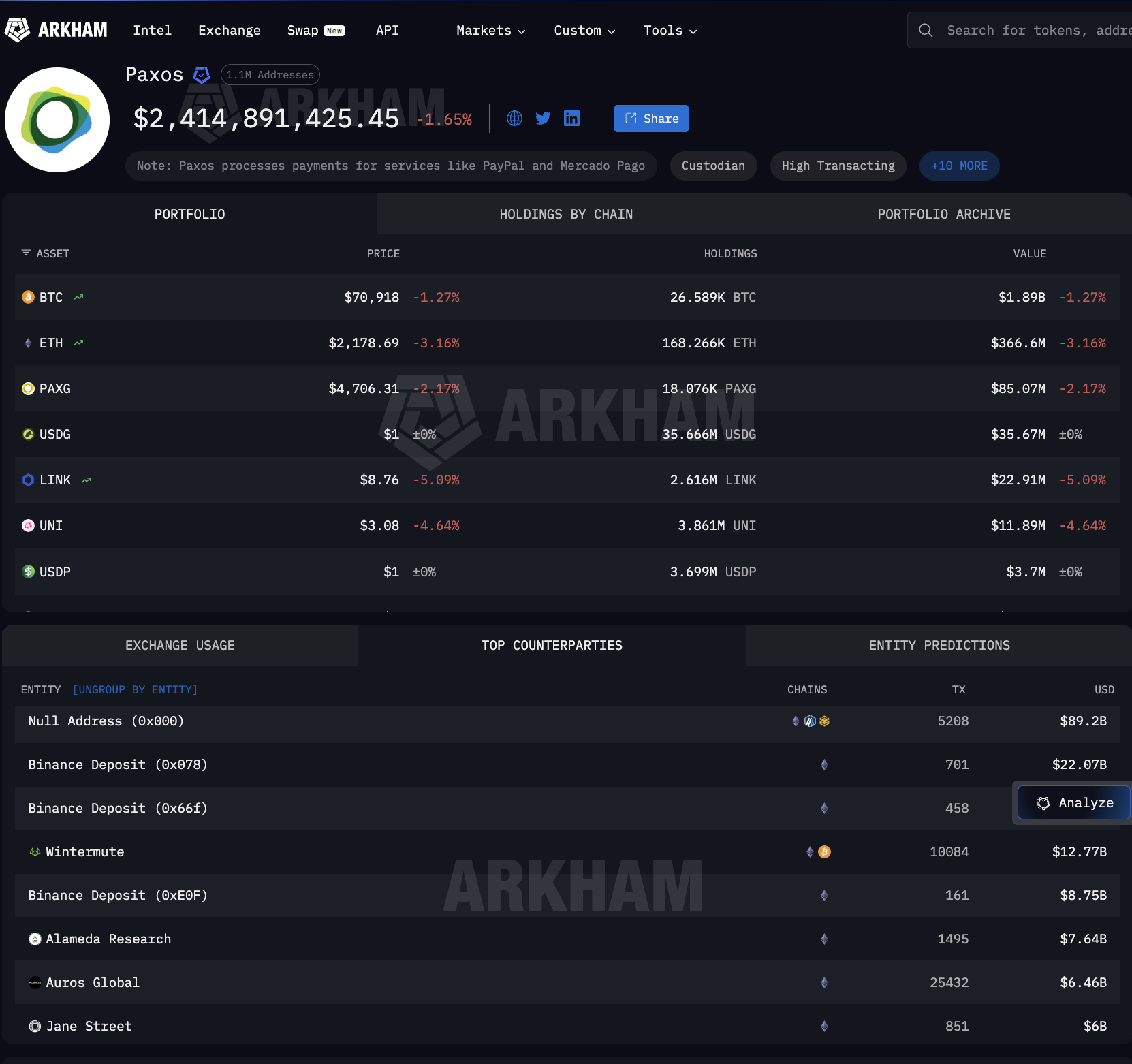

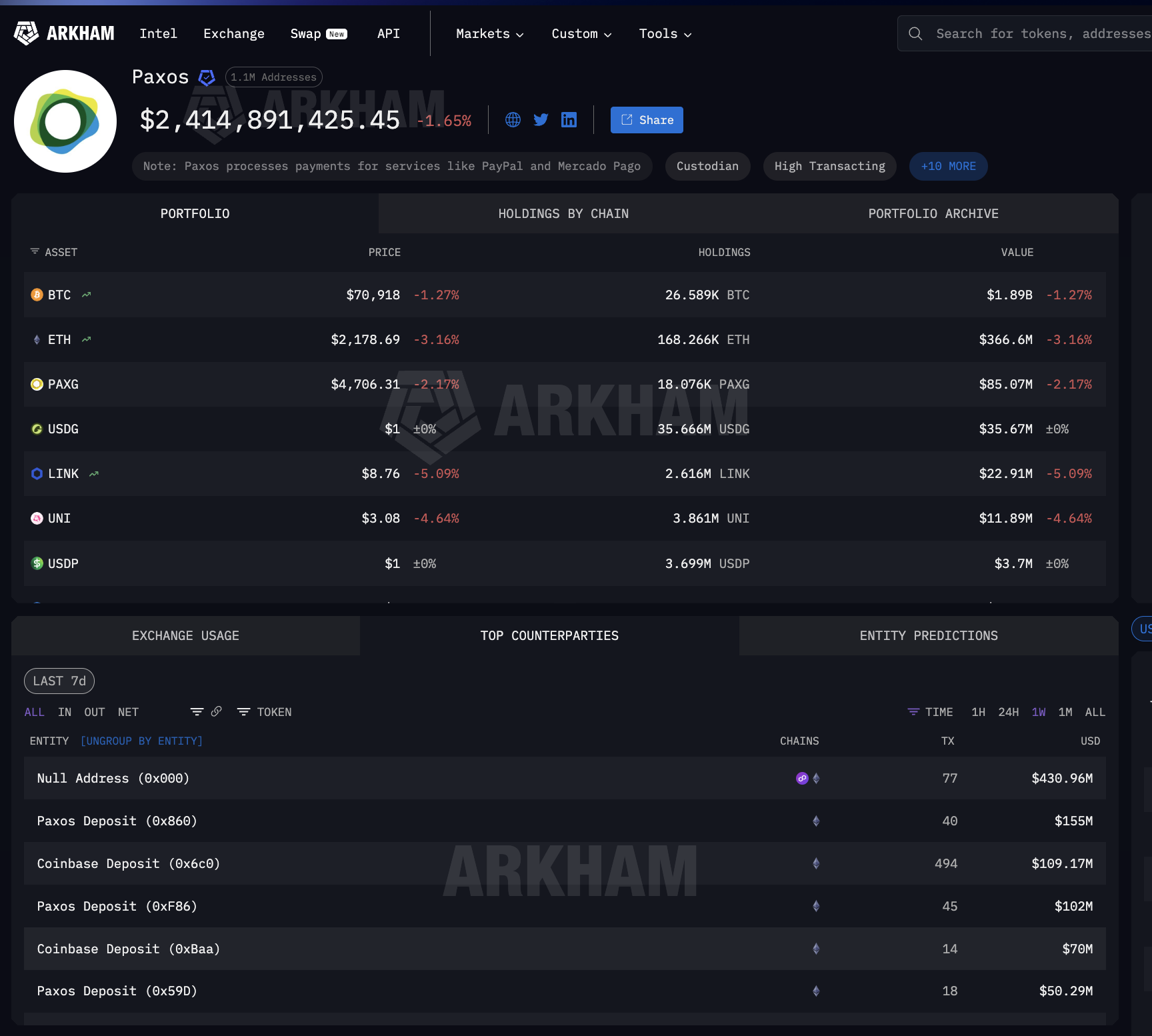

Arkham Intelligence, that great spy in the digital realm, reveals what happens after minting. Paxos has pushed $89.2 billion outward across 5,208 mint-and-burn transactions. The recipients? Not banks, oh no. They are Binance ($22 billion), Wintermute ($12.77 billion), Jane Street ($6 billion), Coinbase ($2 billion), and other titans of the digital and financial worlds. These are not the chains of correspondent banking but the highways of the new economy.

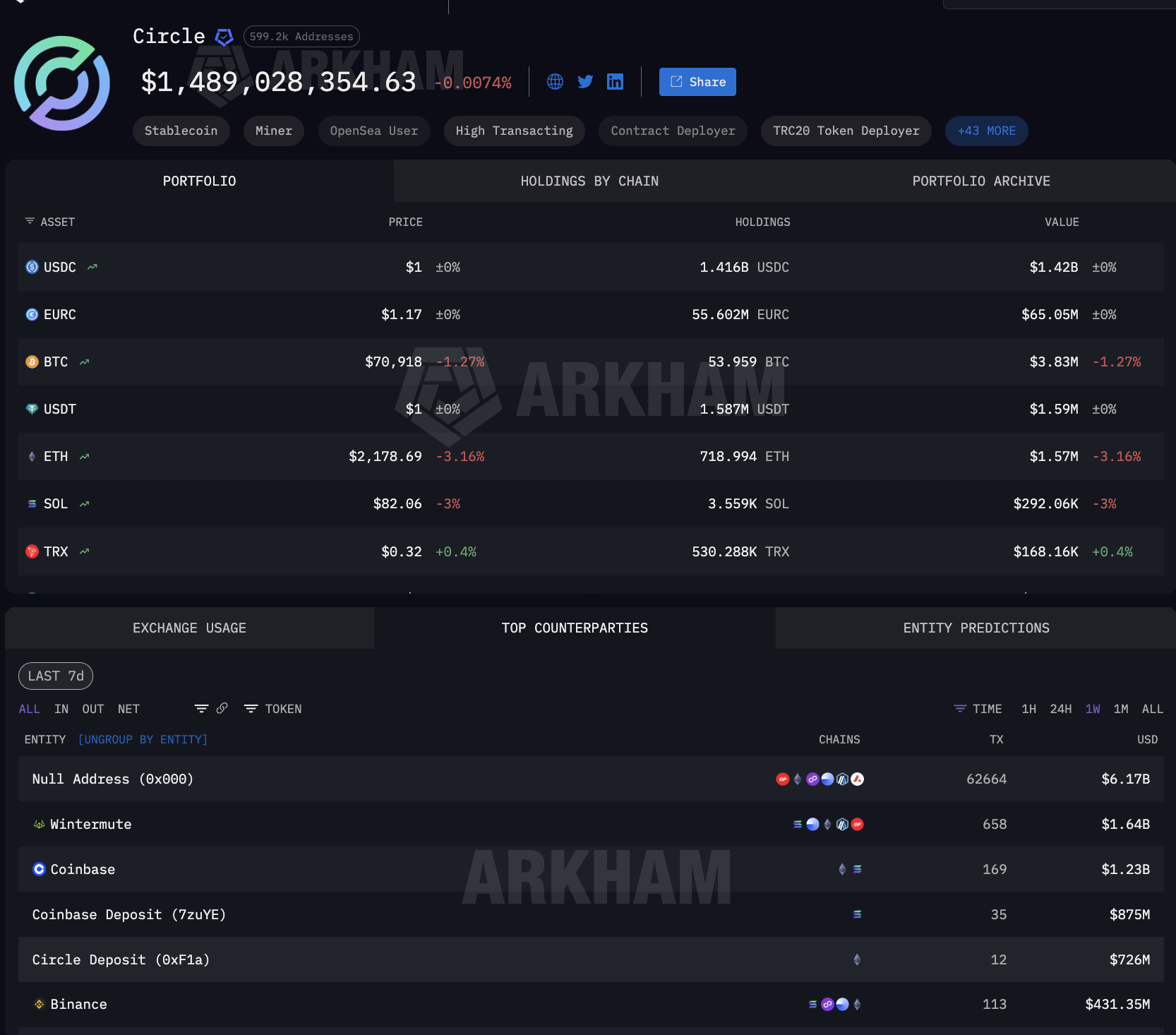

Circle’s counterparty data sings the same tune. $6.17 billion in mint and burn activity. Wintermute at $1.64 billion. Coinbase at $2.1 billion across multiple deposit addresses. Coinbase, that great distributor, straddles both sides of the TradFi settlement market, a Janus-faced entity in this digital drama.

The outflows of Paxos and Circle are dominated by mint and burn operations, the mechanism by which stablecoin issuers create and destroy tokens on demand. The scale of the counterparties reveals where institutional settlement sits. When firms of such magnitude receive billions from Paxos, those funds are freshly minted stablecoins for institutional use-whether to fill a PayPal merchant payout, settle a Mastercard obligation, or provide liquidity for a Visa partner. The stablecoin is created for settlement and redeemed afterward. A cycle of creation and destruction, like the eternal return of Nietzsche’s dreams.

That on-demand cycle does not exist in correspondent banking. That is how stablecoin infrastructure became the settlement rail. But where do those stablecoins sit between minting and burning? Ah, there’s the rub.

Between Minting and Burning: The Custody Layer Holds the Keys

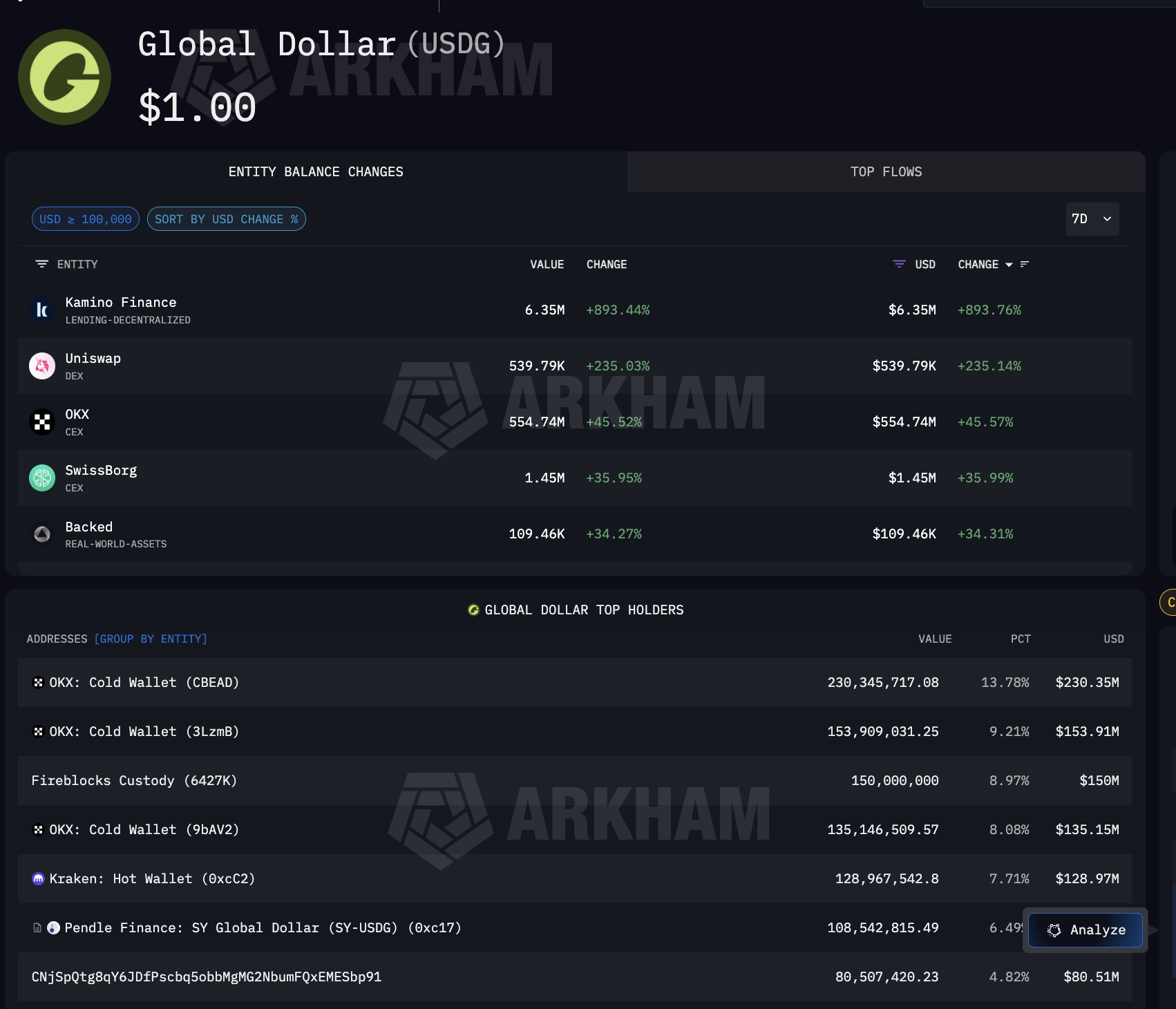

The stablecoin infrastructure serving institutional finance does not merely depend on who mints the tokens. It also depends on where they sit between creation and redemption. USDC, used by millions, makes it difficult to attribute specific holdings to institutional settlement. But USDG, ah, USDG is different. It exists for one purpose: the Global Dollar Network anchored by Mastercard, Robinhood, Kraken, and DBS Bank. Consequently, every large USDG holder is directly tied to that institutional network.

Arkham data on USDG reveals where institutional stablecoins actually sit. The largest single holder is Fireblocks Custody at $150 million, representing 8.97% of the total supply. Alongside Fireblocks, OKX holds $519 million across three cold wallets, while Kraken, a named Global Dollar Network partner, holds $128.97 million. Pendle Finance also holds, indicating that USDG flows into DeFi yield strategies. A web of connections, a tapestry of dependencies.

What makes Fireblocks significant is that it also serves as the custody layer banks use for USDC operations, including on Solana, where Visa settles. In other words, one custody provider sits at the intersection of both the Mastercard settlement rail through USDG and the Visa settlement rail through USDC. A single point of control, a single point of failure? Perhaps, but such is the nature of efficiency.

The full stablecoin infrastructure path is now visible. Circle and Paxos mint. Coinbase, Wintermute, and Jane Street distribute. Fireblocks and exchange cold wallets hold. The reach extends beyond card networks. Arkham’s Paxos entity page confirms that Paxos also processes payments for Mercado Pago, the largest fintech platform in Latin America, meaning the same minting infrastructure serving Mastercard and PayPal also serves emerging market settlement. A global network, built on the backs of a few.

At every step between minting and redemption, institutional finance depends on the same concentrated set of crypto stablecoin infrastructure providers. A single thread, pulling the entire tapestry.

Four Strategies, One Infrastructure

With the settlement stack mapped, the question becomes how institutional finance is actually connected to it. Each major player chose a different strategy. All of them plugged into the same underlying stablecoin infrastructure. A symphony of diversity, built on a foundation of uniformity.

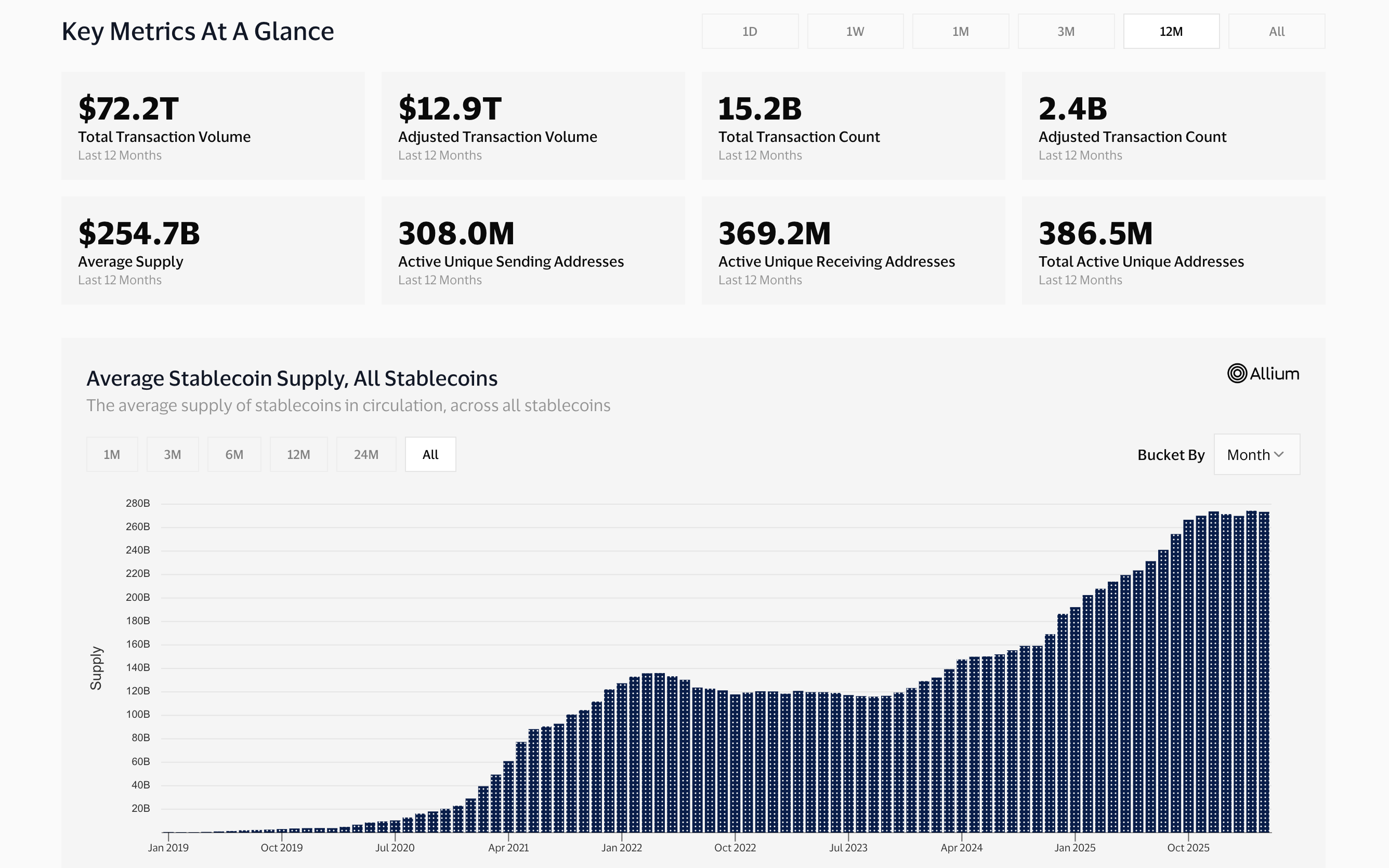

Visa committed the hardest. As of December 2025, it settled $3.5 billion annually in USDC on Solana through Cross River Bank and Lead Bank. It expanded to four stablecoins across four chains: USDC, PYUSD, USDG, and EURC on Solana, Ethereum, Stellar, and Avalanche. Stablecoin-linked cards via Stripe’s Bridge are live in 18 countries, expanding to 100+. Visa also built its own on-chain analytics dashboard with Allium Labs, tracking $12.9 trillion in adjusted stablecoin volume and treating on-chain data as core business intelligence. A behemoth, embracing the new world with open arms.

Mastercard hedged instead, enabling four stablecoins across its network: USDC, PYUSD, USDG, and FIUSD. It joined the Paxos Global Dollar Network for USDG, the same stablecoin held by Fireblocks Custody at $150 million, as shown earlier. A cautious approach, dipping its toes into the digital waters.

Stripe acquired the infrastructure directly, buying Bridge for $1.1 billion. Bridge now powers both the Visa stablecoin-linked cards and Stripe’s own stablecoin financial accounts across 101 countries, running on the same USDC that Circle mints. A strategic move, controlling the means of production.

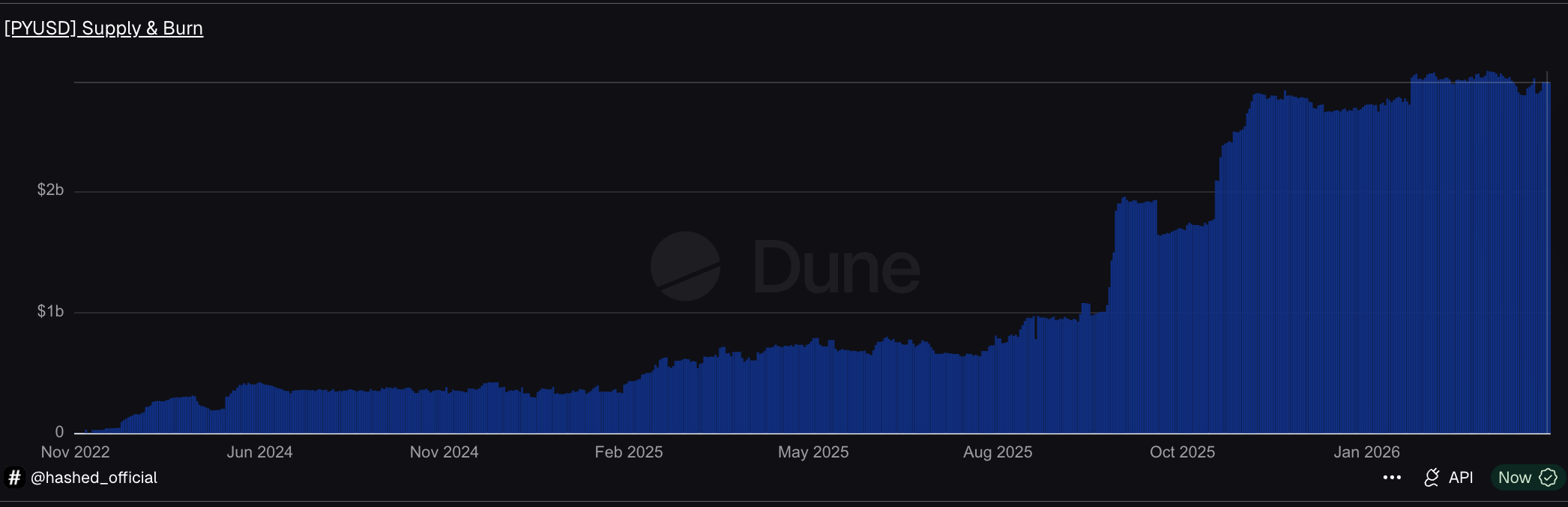

PayPal built its own stablecoin. PYUSD, minted by Paxos, reached $3.95 billion in supply across 70 markets (per DeFiLlama data). On Solana, PYUSD circulates at 0.6x daily velocity, four times its Ethereum rate, concentrating on the same chain that Visa chose. A bold move, creating its own digital currency.

Four strategies. Same stablecoin infrastructure underneath: Circle or Paxos minting, Coinbase distributing, and Fireblocks holding. But everything needs to be linked better. A house of cards, built on a foundation of digital trust.

The Stablecoin Infrastructure Stack: A New Settlement Layer

The evidence across this piece converges into a clear answer. Stablecoin infrastructure became the settlement layer for institutional finance, not because institutions adopted crypto. It became one because a small number of providers built pipes that were faster, cheaper, and available 24/7, and every major institution plugged in rather than building its own. A tale of convenience, of pragmatism, of the irresistible allure of efficiency.

The stack has four layers, each of which is concentrated.

At the supply layer, Circle and Paxos mint the stablecoins that institutional finance depends on. Circle’s USDC moved $8.3 trillion in a single month. Paxos mints for PayPal, Mastercard, and Mercado Pago through the same entity. The alchemists of the digital age.

At the distribution layer, Arkham data shows both minters routing stablecoins through the same counterparties: Coinbase and Wintermute. The settlement rail bypasses correspondent banks entirely. A new order, built on old foundations.

At the custody layer, Fireblocks holds $150 million in USDG as the largest single holder, while also receiving USDC on Solana, straddling both card network settlement rails through a single custody provider. The gatekeepers of digital wealth.

At the integration layer, Visa settles $3.5 billion annually and monitors stablecoin flows as core business intelligence. Mastercard enabled four stablecoins. Stripe bought Bridge for $1.1 billion. PayPal launched PYUSD across 70 markets. JP Morgan settled debt in USDC on Solana. None built new rails. A symphony of adoption, built on a foundation of shared infrastructure.

This mirrors the pattern from our previous analysis of institutional crypto custody, where seven entities across four layers control where crypto sits. Here, a similar concentration controls how institutional money moves. Different function, same structural conclusion: institutional finance is scaling on stablecoin infrastructure built by a handful of providers. The rails exist. The question now is whether the next wave of adoption diversifies that dependency or deepens it. A question for the ages, a question for the future.

Read More

- Brent Oil Forecast

- Gold Rate Forecast

- Silver Rate Forecast

- CNY JPY PREDICTION

- USD BRL PREDICTION

- ETH PREDICTION. ETH cryptocurrency

- Lobsters, AI, and Crypto Chaos: OpenClaw’s Wild Takeover

- Bank of the Nerves: XRP’s Quiet Lament Sparks 63% Jump-Read Why!

- Crypto Whale Bags $2M Profit as Oil Prices Crash on US-Iran Ceasefire News

- Franklin Templeton’s Bold Leap into the Digital Age: Will it Pay Off?

2026-04-13 04:21